What is the maximum mortgage you should get?

Okay, let's be real. Staring at those mortgage calculators, wondering what that absolute max youcouldborrow is... it's exciting, sure, but it's also terrifying. Will you be able to swing it? Will you be house-poor? Is this the start of a beautiful life, or financial ruin looming just around the corner? We've all been there, that dizzying mix of hope and anxiety.

So many folks get tripped up trying to figure this whole thing out. It's not just about what the banksaysyou can afford, is it? It's about juggling all those monthly bills, worrying about future job security, and trying to plan for those curveballs life throws. Banks talk debt-to-income ratios; you're thinking about replacing the water heater and saving for your kid's college fund!

But here's the good news: figuring out asmartmaximum mortgage isn't some impossible math problem designed to keep you up at night. It's about understanding your own finances, your priorities, and what you'rereallycomfortable with. It's about finding that sweet spot where you can build your dream without sacrificing your peace of mind. There are solutions out there, ways to feel confident and in control.

We've all been there, navigating the complexities of homeownership and trying to make the best financial decisions for ourselves and our families. So, let's break this down. We'll ditch the jargon, share some real-world stories, and arm you with the knowledge you need to determine the mortgage that's right foryou. In this article, we're diving deep into what that "maximum mortgage" number actuallymeans, and how to figure out what's realistically – and comfortably – achievable.

My Own Mortgage Rollercoaster

Okay, so picture this: fresh out of college, wide-eyed and ambitious, I wasconvinced I could afford way more house than I actually could. I saw my friends buying places, and I didn't want to be left behind! I went to the bank, got pre-approved for a ridiculously large amount, and started house hunting. I fell in love with a charming Victorian fixer-upper. Then came the reality check. The inspection report was a nightmare – foundation issues, ancient plumbing, the works! Suddenly, that "affordable" mortgage felt like a lead weight. I panicked. I ended up walking away from the deal, losing my earnest money deposit, and feeling completely defeated. It was a hard lesson, but it taught me the importance of doing my homework, not just on the house itself, but on my own financial limitations. That experience is what inspired me to do more research and help others avoid those kinds of mistakes.

What Isthe Maximum Mortgage, Anyway?

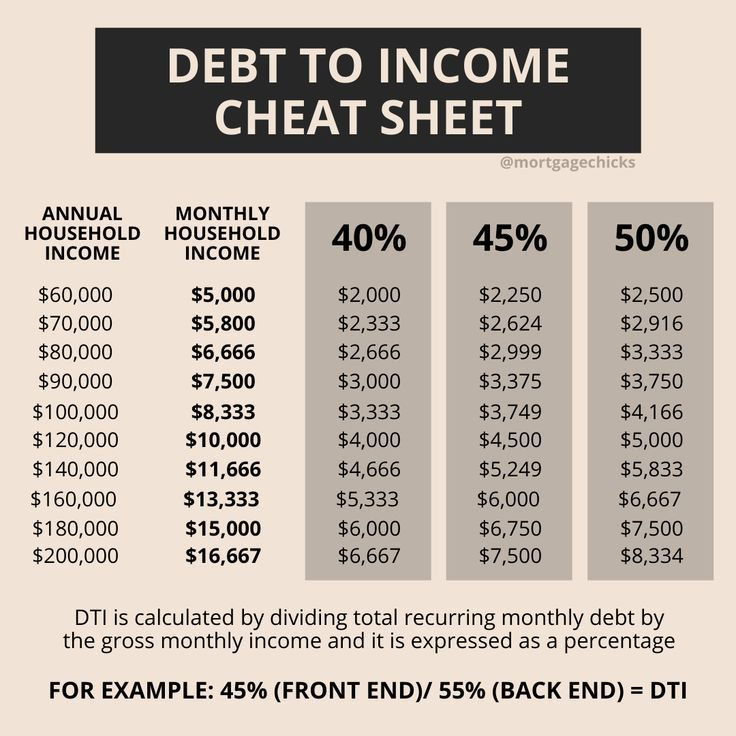

The "maximum mortgage" isn't just a single number a bank throws at you. It's more like the top rung of a very tall ladder. Think of it this way: you're borrowing a ladder (the mortgage) to reach a higher window (your dream home). The bank is trying to gauge how stable you are on the lower rungs before letting you climb all the way to the top. They look at things like your income, your credit score, your debts (car loans, student loans, credit card balances), and your savings. They use these factors to calculate your debt-to-income ratio (DTI) and determine how much they're willing to lend you. But here's the kicker: just because theysayyou can climb to the top doesn't mean youshould. Your comfort level and future financial goals play a huge role. The bank isn't thinking about childcare expenses or those yearly vacations; you are!

Mortgage Myths and Legends

There's this pervasive myth that getting pre-approved for a certain mortgage amount means youhaveto borrow that much. Or that it's evensmartto. Some people feel like they need to max out the amount. I've even heard people say that banks make mistakes on the high side and you don't need to worry about your own budget! Honestly, a good rule of thumb is that the bank wants to give you as much money as possible, and they are much more optimistic than you need to be. Another one: many people think that only a high income or perfect credit guarantees a low interest rate. While those are important, you can improve your chances by shopping around and comparing offers from multiple lenders. It's like shopping for a car – don't settle for the first price you're given. There's a historical element too. Before standardized credit scores, getting a mortgage was heavily reliant on personal relationships and knowing someone at the bank. Now, it's more data-driven, but understanding those historical nuances can help you appreciate the power of building a strong financial profile.

Hidden Mortgage Traps (and How to Avoid Them)

Here’s a secret: small terms can have HUGE consequences. For example, opting for a lower interest rate but adding points can seem appealing initially, but it could cost you more in the long run if you don't stay in the house long enough to recoup the cost of those points. Another hidden trap? Private Mortgage Insurance (PMI). If you put down less than 20% on your home, you'll likely have to pay PMI, which is an added monthly expense that doesn't go towards your principal. Learn to negotiate! Don't be afraid to ask lenders to waive certain fees or match a competitor's offer. You might be surprised at what they're willing to do, especially if you have a strong credit score and a solid financial history. Also, pay attention to the fine print. Those closing costs can add up quickly, so be sure to review the loan estimate carefully and ask questions about anything you don't understand.

Smart Strategies for Choosing a Mortgage Lender

Choosing a mortgage lender is like picking a doctor – you want someone experienced, trustworthy, and who has your best interests at heart. Start by getting recommendations from friends, family, or your real estate agent. Then, do your research and read online reviews. Check their ratings with the Better Business Bureau. Don't be afraid to shop around and get quotes from multiple lenders. Compare not just the interest rates, but also the fees, terms, and customer service. Ask lots of questions! Find out about their loan options, their application process, and their closing timeline. Pay attention to how responsive and helpful they are. Do they explain things clearly and patiently? Or do they pressure you to make a decision? Trust your gut. If something feels off, move on. You're making a huge financial commitment, so you deserve to work with someone you feel comfortable with.

Key Mortgage Details to Know

Here are some essential details you'll need to know: Credit Score Requirements: A higher credit score typically means a lower interest rate. Check your credit report regularly and address any errors or discrepancies. Types of Documents: Be prepared to provide proof of income (pay stubs, tax returns), bank statements, and identification. Timelines:The mortgage process can take anywhere from 30 to 60 days, so be patient and stay organized.

Actionable Tips for a Smooth Mortgage Process

Want to increase your chances of mortgage success? Here are some insider tips: Apply on Wednesdays: Believe it or not, some studies suggest that applying for a mortgage mid-week can increase your chances of approval. Avoid Applying After a Recent Credit Check: Too many credit inquiries can ding your credit score, so space them out. Talk to the Loan Officer in Person (If Possible):Building a personal connection can help you get personalized advice and potentially negotiate better terms.

Lesser-Known Loan Options

Beyond the traditional mortgage, explore these possibilities: Government Aid (FHA, VA): These programs offer lower down payments and more lenient credit requirements for eligible borrowers. Cooperative Loans: If you're buying into a co-op, you'll need a specific type of loan designed for co-op purchases.

Fun Mortgage Facts (Did You Know?)

Did you know that the average mortgage size varies significantly by country? In some places, it's common to borrow several times your annual income, while in others, people prefer to put down a much larger down payment. And speaking of weird reasons for taking out loans... from funding destination weddings to buying exotic pets, people borrow money for all sorts of things! (While I don't necessarily recommend those options, it highlights the range of needs that mortgages can serve!).

My "How To" Guide to Finding Your Perfect Mortgage Amount

Here's what worked for my cousin, and it might work for you, too. He sat down with his partner and they wrote downeverythingthey spent money on for three months. Every coffee, every streaming service, every impulse buy. Then, they categorized those expenses into "essentials" and "non-essentials." Finally, they ruthlessly cut back on the non-essentials and used that extra money to pay down their existing debts and save for a larger down payment. This did two things: it made them more appealing to lenders, and it gave them amuchclearer picture of what they could realistically afford each month.

"What If" Mortgage Scenarios

Let's face it, life happens. What if you miss a mortgage payment? Contact your lender immediately and explain the situation. They may be able to offer a forbearance plan or other assistance. What if you get scammed? Report it to the authorities and try to recover your funds. What if you want to refinance? Shop around for the best rates and terms and consider whether it makes financial sense to pay the closing costs. Staying informed and proactive is key to navigating these challenges.

Top 5 Smartest Mortgage Decisions I’ve Seen

Here's a curated list based on my experiences:

1.Overpaying Your Mortgage: Contributing even a little extra each month can significantly shorten the loan term and save you thousands in interest.

2.Shopping Around for Insurance: Don't just go with the first homeowners insurance policy you're offered. Compare quotes from multiple providers to find the best coverage at the best price.

3.Building an Emergency Fund: Having a cushion of savings can help you weather unexpected expenses and avoid falling behind on your mortgage payments.

4.Refinancing Strategically: If interest rates drop, refinancing can save you money, but be sure to factor in the closing costs.

5.Seeking Professional Advice: Don't be afraid to consult with a financial advisor or mortgage broker. They can provide personalized guidance and help you make informed decisions.

Mortgage Q&A: Your Questions Answered

Here are a few questions I get asked a lot: Friend:"Is it better to go with a fixed-rate or adjustable-rate mortgage?" Me: "That depends on your risk tolerance and how long you plan to stay in the house. Fixed-rate mortgages offer stability, while adjustable-rate mortgages can be cheaper initially but could increase over time."Friend: "How much should I save for a down payment?" Me: "Ideally, 20% to avoid PMI, but there are loan options available with lower down payments. Just be prepared to pay PMI until you reach 20% equity."Friend: "What's the difference between pre-qualification and pre-approval?" Me: "Pre-qualification is a quick estimate based on limited information, while pre-approval involves a more thorough review of your finances. Pre-approval carries more weight when you're making an offer on a house."Friend: "Is it okay to take out a loan to cover the down payment?" Me: "This is generally not recommended, as it increases your debt burden and can make it harder to qualify for a mortgage. It's better to save up for the down payment."

Conclusion of What is the maximum mortgage you should get?

So, there you have it. Figuring out the "maximum mortgage" you should get is about way more than just what the bank is willing to lend you. It's about knowing your own financial landscape, understanding the potential risks and rewards, and making a decision that aligns with your long-term goals. Don't be afraid to ask questions, do your research, and seek professional advice. Remember, you're in control of this process. Take your time, be smart, and choose the mortgage that allows you to build your dream without sacrificing your peace of mind. Happy house hunting!